Tax Affinity Accountants with their high street branches The Smart Move: Why You Should Use a Tax Accountant for Your Self-Assessment

In the world of personal finance, few things are as certain as taxes. Each year, individuals across the globe prepare to navigate the labyrinth of tax regulations, deductions, and forms required for their self-assessment. While some opt for the DIY approach, a growing number are discovering the numerous benefits of enlisting the expertise of a tax accountant. In this blog post, we'll explore why using a tax accountant for your self-assessment is not just a smart choice but often a financially savvy one. 1. Expertise and Knowledge: Tax accountants are professionals who specialize in tax laws and regulations. They stay up-to-date with the latest changes in tax codes and have the experience to navigate complex financial situations. This expertise can help you minimize your tax liability legally. 2. Maximize Deductions and Credits: Tax accountants have a keen eye for identifying deductions and credits that you might overlook. Their attention to detail can result in significant savings, ensuring you're not paying more taxes than necessary. 3. Reduce Stress and Save Time: Preparing your own taxes can be time-consuming and stressful. It often involves sifting through a mountain of paperwork and deciphering intricate tax jargon. Hiring a tax accountant frees up your time and reduces the stress associated with tax season. 4. Avoid Costly Mistakes: Filing taxes incorrectly can lead to penalties and audits. Tax accountants are trained to minimize errors and ensure that your return is accurate, reducing the risk of costly mistakes that can haunt you later. 5. Year-Round Assistance: A tax accountant's support isn't limited to just tax season. They can offer financial advice throughout the year, helping you make informed decisions to optimize your tax situation and financial health. 6. Audit Protection: If you're audited by tax authorities, having a tax accountant on your side can be invaluable. They can guide you through the audit process and ensure that your rights are protected. 7. Customized Strategies: Tax accountants can create personalized tax strategies that align with your financial goals. They consider your unique circumstances to help you make the most of available tax benefits. 8. Peace of Mind: Perhaps one of the most valuable aspects of hiring a tax accountant is the peace of mind it brings. Knowing that a professional is handling your taxes can alleviate anxiety and allow you to focus on other aspects of your life. 9. Cost Savings: Contrary to common belief, hiring a tax accountant can often result in cost savings. The deductions and credits they can uncover, combined with the reduction in errors, can more than offset their fees. 10. Legal and Ethical Compliance: Tax accountants operate within the bounds of the law and adhere to ethical standards. This ensures that your taxes are filed ethically and legally, eliminating any worries about potential legal repercussions. In conclusion, the decision to use a tax accountant like Tax Affinity for your self-assessment is an investment in your financial well-being. Their expertise, ability to maximize savings, and dedication to compliance can make the process smoother, more accurate, and less stressful. Ultimately, it's a smart move that can pay dividends in terms of both financial savings and peace of mind. So, this tax season, consider enlisting the help of a tax accountant like Tax Affinity and reap the rewards of a stress-free and financially optimized experience. By Anni Khan at Tax Affinity Accountants Tax Affinity Accountants are the number rated and recommended Tax Accountants in London. With branches in Worcester Park and Kingston upon Thames and Epsom and Ewell they are considered in the Industry to be expert business accountants and tax advisors for both individuals and small & medium sized businesses (SME's). Helping and supporting both individuals and limited company owners / self employed people throughout the UK and the world, they regularly help clients grow their business providing tailored advice and support. Their support has been considered invaluable by many clients and key to their success. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

0 Comments

With only a few working days left. This is an important reminder that if you have not already had your 2021-22 personal tax return done. All 21/22 tax returns (self assessments) need to be calculated & submitted to HMRC before the 31st January 2023 and any tax payable for the year to be paid by that date also. And we recommend this is urgently done and you contact us today. If you had it done or do not need it then ignore this reminder.

As per last year HMRC is saving money & will not send postal reminders. They now choose instead to collect money through letters of fines for missed deadlines saying 'all tax payers should be aware of the self assessment deadline, and not expect HMRC to remind them'. With fines starting at £100 rising to £1300 plus interest for late filing and payment even if you had no tax to pay, there really is no excuse to not have it done as soon as possible so get in touch today and ensure its calculated and declared by professional tax accountant, someone who will make sure to look after your best financial interests while freeing you up to concentrate on the things your love. To complete the 2021/2022 self assessment you will need the following information:

Tax Affinity Accountants are experts Business, Tax and Accountancy. With branches in Worcester Park and Kingston upon Thames and Epsom and Ewell they are considered in the Industry to be expert business accountants and tax advisors for both individuals and small & medium sized businesses (SME's). Helping and supporting both individuals and limited company owners / self employed people throughout the UK and the world, they regularly help clients grow their business providing tailored advice and support. Their support has been considered invaluable by many clients and key to their success. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.  Tax Affinity have many high street branches HMRC relishes the idea that tax payers will make errors in their tax returns and then they will pay higher taxes or be fines for making errors. The number of errors by members of the public doing their own self assessments has been rising steeply in the last few years and HMRC has been raking in fines for errors. So its very important to try to ensure you make none.

Why? - Well simply mistakes on your tax returns could cost you a lot of hard earned money. Solution? - Avoid HMRC penalties and charges by making sure you don’t commit these mistakes during tax return time by getting an expert like Tax Affinity Accountants (one the most highly recommended accountants in the UK) to do calculate and submit the return for you and sleep easy at night knowing you paid the least tax and everything was correct according to HMRC rules. Key things to keep in double check:

A good tax accountant should save you much more in tax than what he/she charges. And having a Tax Affinity accountant calculate your personal and business tax situation will lead to zero mistakes on your return and a lower tax bill first time every time. Fill out our contact us page to find an office near you and we will be happy to help you sleep easier at night. By Anni Khan at Tax Affinity Accountants Tax Affinity Accountants are experts Business, Tax and Accountancy. With branches in Worcester Park and Kingston upon Thames and Epsom and Ewell they are considered in the Industry to be expert business accountants and tax advisors for both individuals and small & medium sized businesses (SME's). Helping and supporting both individuals and limited company owners / self employed people throughout the UK and the world, they regularly help clients grow their business providing tailored advice and support. Their support has been considered invaluable by many clients and key to their success. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends. Last year over 30,000 people filed their tax returns between christmas eve and boxing day12/19/2021  Tax Affinity Accountants have branches local to you Did you know last year more than 30,000 people in the UK did their tax return between Christmas Eve and Boxing Day?

As of writing this, there are only 20 working days left until HMRC's self assessment deadline of 31st Jan 2022. Each year millions of people leave their tax return (self assessment) to the last minute and then stress out if they declared the info correctly and if the tax due is correct. Statistically the number one worry tends to be if their submission may trigger an HMRC investigation into their tax affairs... death and taxes being the fear we suppose. Plus in the last tax year due to Covid 19 and lockdown's there were many other sources of income e.g. council support grants, SEISS (self employed grants), furlough, bounce back loans, universal credit, tax credits etc. Making tax returns more complicated and resulting with higher taxes due for most tax payers. If your worried we recommend you get in touch with one of our tax experts. Because we have seen a lot more investigations this year than previous years as HMRC starts it claw back to try to shore up the UK government income and focuses even more on tax avoidance and incorrect information. So if you have not had your 2020/21 (6.4.20 to 5.4.21) tax return (self assessment) completed then you urgently need to get in touch today as the number of working days are fast decreasing and before you know it the time will be gone and you may end up facing badly caclulated tax return paying more tax than you need to or worse a fine by HMRC for missing the deadline. Contact us today by clicking this link or calling us on the number above. And share this page with your friends and family. By Anni Khan at Tax Affinity Accountants Tax Affinity Accountants are experts in Tax and Accountancy. With branches in Worcester Park and Kingston upon Thames and Epsom and Ewell they are considered in the Industry to be expert business accountants and tax advisors for small and medium sized businesses (SME's). Helping and supporting limited company owners and self employed people throughout the UK, they regularly help clients grow their business providing tailored advice and support. Their support has been considered invaluable by many clients and key to their success. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.  Some landlords wrongly think by not declaring their property to HMRC they are safe! As experts in property tax we often get asked by clients who are landlords and property developers how to save tax - especially so as the cost of letting a property rises year on year.

With our experience and special insider knowledge that HMRC in 2014 - 2015 is especially looking at checking landlords who are not declaring the correct rental income and correct capital gains on second homes. This is something that is becoming more important as people realise it is harder and harder to hide their untaxed property incomes. Landlords or their accountants are required to fill the the land and property section on their self assessment tax return showing all the rental business income they have made and as many want to make sure they pay the least amount of tax possible. We have have created a simple list to help guide you. Here are Tax Affinity Accountants top tips to save property tax. 1. Claim for all your property related expenses. Its important to make sure you claim for all your expenses when submitting your tax return. These should include: • Travel costs incurred when travelling back-and-to the investment property • Estate Agent or private advertisement costs • Mobile or landline telephone calls made (or text messages sent) in connection with the rental property • Payments for safety certificates eg Gas Safety • Bank charges (i.e. overdraft, interest on mortgage) • Professional fees e.g. Architect, Solicitor, Accountant etc • Monthly payments to property investment related products and services eg Insurances etc 2. Dividing your rental income between partners. A top tip is to consider putting your buy-to-let property into joint named ownership. Then the total income can be divided into each person's income and multiplying the personal allowance claimable on the income. 3. Claim all empty period expenses. Often there are periods between lettings that the buy-to-let property is empty and the owner has to pay for council tax or utlity bills. These should be noted and claimed. 4. Claiming the home office allowance. £4 per week (ie £208 per year) can be claimed for the use of your home to manage and run your rental property income. This amount can be claimed without evidence and more can be claimed if it can be justified. 5. Interest and finance costs. Most properties are on mortgages and the interest part of any mortgage is claimable as an expense. So if you have an interest only mortgage then the whole amount is claimable per month paid. Often landlords also forget to claim for money borrowed from friends or family or taken on a credit card or personal loan for the buy-to-let property and the interest on these can also be claimed. The principal can only be claimed when selling the property against capital gains tax. 6. Dont forget to carrying forward loss from previous year Most of the time a new buy-to-let property will not breakeven in its first year and so many landlords have significant rental losses for that year. Then when they start to make income from the property most forget about this loss which can be offset against the current years income. This could even mean no tax to pay in the current year if the losses are great enough. This requires detailed technical knowledge and so any lanldord in this situation should contact an experienced accountant such as Tax Affinity Accoutants. 7. Capital gains avoidance If landlords who are planning to sell their property, need to plan months or even a year ahead to increase their options of minimising capital gains tax which will arise on the sale of the property. This is usually best done getting expert advice from an accountant experienced in tax and property such as Tax Affinity Accountants. What top property developers and landlords know that mostly the fees paid to a good accountant are far less in comparison than the tax he/she will save you. 8. Wear and tear allowance Letting your property as furnished as opposed to unfurnished can allow you to claim up to 10% of the gross income as a valid expense for the upkeep and repair of furtniture in the tax year. 9. Make Sure to avoid HMRC interest and penalties Sound obvious but far to often, we see penalties and interest charges for late filing of tax returns and missed deadlines for documents to HMRC. The deadline for a paper return to HMRC is 31st Oct and online 31st Jan each year. Please also not that landlords will not be able to submit their return electronically if there are any capital gains elements on the return. ie the sale of any property. An experienced accountant needs to be contacted for this purpose which if knowledgable enough could ensure all capital expenditure is claimed to reduce the capital gains liability as low as possible. By Andrew at Tax Affinity Accountants. Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered to be property tax experts helping and supporting ladlords across the UK. They regularly help new landlords and property developers and provide valuable ongoing support. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends. CIS: Sub-contractor Tax in the construction industry The Construction Industry Scheme, CIS, details payments for sub-contractors from contractors. As the name suggests, it is only applicable in the construction industry. When a contractors needs work from a different skills set (like an electrician, plasterer or plumber), the person(s) they ask to complete the work will be a sub-contractor. The rules as to what qualifies as construction are complex and it worth seeking professional advice to ensure you are not over paying tax. If you are a sub-contractor in construction, you need register under CIS and be registered as self-employed. As the contractor gets a sum of money for the work as an entirety, it is the contractor who is responsible for paying the sub-contractor. As it is a service based position, income tax and NI contribution are taken off the wage of the sub-contractor by the contractor and paid to HMRC at a rate of 20% of the total pay. The tax year for any sub-contractor or self-employed persons is 6th April until 5th April the following year. During this time, all gross pay and deductions will be added together to work out a total pay. Then the profit for the sub-contractor will be worked out after deducting cost of materials and then any other business expenses such as training, travel or phone bills from the income. If, at the end of the year, the contractor is below the personal allowance threshold (£9,440 for the year ending 2014, going up to £10,000 for the year ending 2015) they will not have to pay any tax. Therefore any tax paid by contractors to HMRC out of the sub-contractors pay will be refundable. See below example for Mr J Bloggs, a plasterer:

As we can see, the profit for the year is below the personal allowance for the year ending 2014 (£9,440). Therefore, Mr J Bloggs should not have paid any CIS deductions so he is able to reclaim the £2,400 from HMRC at the end of the year. See below example for Mrs J Smith, an electrician, when the profit for the year is above the personal allowance:

In the above example, the profit for the year is above the personal allowance by £5,360. Therefore tax paid should equal 20% of £5,360, which is £1,072. However, we have paid £4,400 from CIS Tax deductions. This means that Mrs J Smith is eligible for a Tax refund of £3,328. The same tax rules apply for sub-contractors and self-employed persons as those in employment meaning when you hit the upper threshold (£41,450 in the year ended 2014 rising to £41,865 for the year ending 2015) you will have to pay 40% tax on that amount. The summary is below, using the 2015 figures:

To try to make the above simpler, we will look at how much tax should be paid by Mrs O McKenzie who had an income (profit) for the year of £55,000:

If all of her income came from sub-contracting, the amount of CIS Tax already paid would be 20% of £55,000 which is £11,000. She is due to pay £11,627 so she would have to pay HMRC an extra £627 to avoid a potential fine in the future for Tax Evasion. This profit figure is very high so most sub-contractors who register under the CIS as self-employed will get a tax refund. It is advisable that if you qualify for this scheme, you do so as it will more often than not result in you getting money back from HMRC at the end of the tax year. There are also National Insurance (NI) contributions that need to be paid. These are more complicated as the amount you pay will vary with the amount of profit you have at the end of the year. There are different classes and different personal allowances depending upon what type status of employment you have and what your level of income is. It is worth seeking a professionals help at this point to ensure you do not make a mistake and pay the wrong amount. If you are still confused, or think that you should get a refund, and want to know what the next step is, get in contact with us here at Tax Affinity. Use any of the contact details on the website and we will gladly assist you on the next stage. By Owen Cain at Tax Affinity Accountants

How to save Money on Capital Gains Tax

How do you save money on Capital Gains Tax? For an Accountant this is a question which is asked regularly. But as you can always find a way to save money. Below I give you a basic insight into how CGT (Capital Gains Tax) works, some tips, exceptions and how to avoid it completely:

How does it work? CGT is run through the tax year (6th April one year to 5th of April the following year). It is worked out on the total of your taxable profit from any capital assets that you hold. For instance, property, bonds and shares on the stock exchange. Furthermore, it is when the amount exceeds the purchase price of a property, bond and shares/stock. The amount that is exempt (tax free) annually is £10,900 for 2013 to 2014 (which increases to £11,000 for 2014 to 2015). At present there are two different types of CGT. The basic rate taxpayers pay is 18%, although the higher rate tax payers pay is 28% and if the capital gains goes over your threshold you will pay the higher tax. Tips to save money Below are some tips to keep the CGT Low as possible:

Exceptions Any profit made on selling your home is tax exempt, unless you did one of the options below:

You can also get away with not paying tax if you make a profit on selling a car, ISA’s, Peps, UK government gifts, savings certificate, premium bonds, personal belongings that are worth £6,000 or less when you come around to selling them. Furthermore there is a 10% tax rate with the entrepreneur’s allowance, which is aimed to help people that are selling their businesses they have built up. It has a lifetime limit of £5m. Avoid it completely If you want to avoid paying the higher threshold of 28% there are some suggestions below:

You can defer your CGT by reinvesting it into the Enterprise Investment Scheme (EIS). You would have a limit of £200,000. Furthermore, any profit made will be exempt if you meet the qualifying standards. Finally, while tax avoidance is legal, tax evasion is illegal. So do not be tempted to sell assets without declaring any profit to HMRC. Defrauding the tax man can land you with a large fine or even a prison sentence. But the advice and support of an experienced tax accountant and some sound forward tax planning can save you thousands of pounds. By Tahir Malik at Tax Affinity Accountants Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered in the Finance Industry to be the experts in all types of Tax including Capital Gains Tax. Helping and supporting businesses and individuals throughout the UK, they regularly help people with their CGT tax issues. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

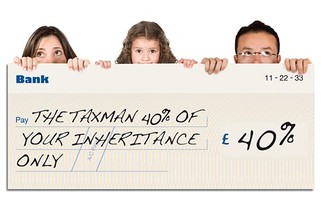

Plan Plan Plan ahead to save Inheritance Tax

Saving Inheritance tax

Inheritance tax can be a tricky issue to deal with for most people but it is generally considered a “voluntary tax” as good tax planning can greatly reduce your inheritance tax liability or erase it completely. Assets exceeding the current inheritance tax threshold of £325,000 (for tax year 13/14) are taxed at 40%. That’s basically half of your excess assets going straight to the government and not to your loved ones. This is why inheritance tax can be extremely costly for those who have not done sufficient planning. Fortunately, there are many exemptions and allowances to utilise which would significantly reduce the amount of inheritance tax you have to pay. Here are a few things to consider that can help you save some inheritance tax:- Make a Will Making a will allows you to know that your estate is divided exactly as you want it to be when you die. In the absence of a will, people that you wish to benefit from your estate such as an unmarried partner may not be entitled to any share in the event of intestacy. What is a gift? A gift is something of value given unconditionally to someone without any reservations. The biggest asset that most people are in possession of is their house. However, giving away your house yet trying to live in it may allow HMRC to invalidate the gift as genuine and apply tax on it. Give away sooner Majority of gifts you make are classified as “potentially exempt transfers”. If you survive more than seven years after making the gift, no inheritance tax is due on that gift. The amount of tax can be reduced depending on how long you lived after making the gift due to taper relief. Gifts made less than three years before death have no reduction in tax. If the gift was made three to four years before death then tax is reduced by 20%. This increases by 20% for every extra year the donor lives up to seven years where the whole amount is exempt. Therefore it can help relief some financial burden on your death estate if you make gifts sooner rather than later. Allowances to take advantage of You can give away gifts worth up to £3,000 in total per person every tax year and these gifts will be exempt from inheritance tax when you pass away. Any unused part of this annual allowance can be carried forward to the following year, but if you don’t use it in that year, the carried-over exemption expires. You can also give up to £5,000 to your children when they marry as a wedding gift. Grandparents can give up to £2,500 and others up to £1,000. Regular Gifting Regular gifting can dramatically reduce your inheritance tax bill as long as they meet the following criteria: they must be from your income, they must be regular and they must not decrease the standard of living of the donor. Be generous on birthdays Gifts under £250 to any recipient per tax year are exempt from inheritance tax. This means that it might be worth giving your boy a big birthday present even if he’s been naughty as it helps reduce the tax bill. Gifts to charities and political parties are tax-free It’s good to know that any donations you make to charities or political parties are inheritance tax free at least. Getting Tax Advice While it is generally more economical for you to do things by yourself, if you have sizeable assets then seeking professional tax advice is well worth your money. You may end up paying a few hundred pounds to potentially save over hundreds of thousands of pounds. I’m no bargain hunter but that sounds like a good deal to me. By Wilson Law at Tax Affinity Accountants Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered in the Finance Industry to be the experts in all types of Tax including Inhertance Tax. Helping and supporting business and individual throughout the UK, they regularly help people with their Inhertance tax issues. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

Wondering if you should you stay a sole trader or register your own limited company?

Sole Trader v Limited Company

A difficult question that the self-employed face is whether to trade as a sole trader/partnership or to trade as a limited company. However, the answer isn’t definitive and is dependent on many factors ranging from the type of business you are running to the type of person you are. Whichever one you choose has different implications for tax, legal and financial responsibilities. The aim of this article is to give you an insight to the advantages and disadvantages in terms of tax purposes of being a sole trader/in a partnership or forming your own limited company. Hopefully it will inform you on the structure most beneficial to you. Legality As a sole trader, you are the business. You have full control and ownership of the business and are able to manage it in any way you like. On the contrary, a limited company is its own legal entity. Instead you serve the company as a director of the company and act as a shareholder. In most cases, you are considered as an employee but this status is not automatically granted in terms of Employment Law, the National Minimum Wage or for Tax Credits. Tax – Sole Trader You are subject to income tax on the taxable profits of your business. For the tax year 2013/14, you pay 20% tax on income between £0 - £32,010 and 40% tax on income between £32,010 - £150,000. Income above £150,000 is taxed at 45%. The personal allowance amount for persons aged under 65 is £9,440. You are also required to pay Class 2 & 4 National Insurance contributions (NIC). Class 2 NIC are at a flat rate of £2.70 per week. However, you may not need to pay Class 2 NIC if your earnings are below £5,725 for the whole year. Visit http://www.hmrc.gov.uk/working/intro/class2.htm to see if you may be exempt from paying Class 2 NIC. Class 4 NIC is calculated based on your profits for the year. For 2013/14, you pay 9% on annual profits between £7,755 and £41,450 and then 2% on any amount over that. Any trading losses you incur on your business can be offset against other your income to reduce your tax liabilities. Tax – Limited Company For a limited company, it pays corporation tax on its taxable profits. Company tax rates are lower than the higher rates of income tax. If you are employed under your company and taking a salary, your earnings from that employment are subject to income tax and Class 1 NIC due through PAYE (Pay As You Earn). The amount you pay is dependent on your earnings. Shareholders of the company who are on a higher tax bracket may have to pay higher a higher tax rate on any dividend income they receive. Losses from the company can only be offset against its other income but not against your income as an individual. What does it all mean? Now for most people, the above two paragraphs may have been not only been of little help but confused you further. Here is a scenario that will make things easier to understand and hopefully give you enough information to aid you in that important decision. You have a trading income of £16,000 pre tax and wish to extract all the profits for yourself. As a sole trader, you will be taxed at 20% for any income in excess of your personal allowance. The total tax liability including the Class 2 & 4 NIC amounts approximately to £2,181 (assuming 48 weeks and available personal allowance of £9,440). The tax calculation for a limited company is slightly more complex as you have more flexibility in how you distribute the income. For simplicity sake, you take the minimum annual wage that is not liable for PAYE tax or NIC which is around £7,000. Company profits under £300,000 are taxed at a rate of 20%. Taxable profits is £9,000 and amounts to a corporation tax liability of £1,800. This leaves £7,200 to be distributed as dividend which is taxed at 10% for income below the earnings threshold of £32,010. The total tax paid equates to £2,520. In this scenario, it is marginally better to see that remaining as a sole trader is more beneficial as you pay much less tax. However, calculations may differ depending on the trading income and how much salary you take. The general idea is that as your trading income increases, its becomes more and more beneficial to trade as a limited company than as a sole trader (40% income tax versus 20% corporation tax). Just a Final Note You are better off trading as a sole trader for tax purposes if your annual trading profits are not high. However, many businesses opt to form limited companies for reasons that extend past tax issues. Should the business fail, you will not be personally liable for its debts if you were a limited company. If you plan to sell the business after a few year then limited is again a better choicAlso if you plan to expand the business then getting finance for your business may be easier if you were a limited company. There are many varying circumstances that makes being one more appealing than the other but if you still appear unsure then just contact us and we’ll be sure to offer you tailored expert advice to aid your decision. By Wilson Law at Tax Affinity Accountants Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered in the Finance Industry to be the small business experts. Helping and supporting business throughout the UK, they regularly help new and established businesses with valuable support. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

BUDGET 2014 HIGHLIGHTS

PERSONAL ALLOWANCE The personal allowance is the amount of income you can receive each year without having to pay tax on it. This amount is to increase to £10,000 for 2014/15 and to £10,500 for 2015/16. The basic rate taxpayer will see a saving of about £112 in 2014-15 and a further £100 in 2015-16 on their annual income tax bill. HIGHER RATE TAX PAYERS The threshold for which individuals pay tax at the higher rate of 40% will increase by 1% for both tax years. ANNUAL INVESTMENT ALLOWANCE For businesses, the annual investment allowance will increase from £250,000 to £500,000 until 31 December 2015. HIGHER ANNUAL SUBSCRIPTION LIMIT FOR INDIVIDUAL SAVINGS ACCOUNTS FROM 1 JULY 2014 The chancellor has announced big changes to the Individual Savings Accounts (ISA). The new policy means that, from July onwards, it will be possible to save up to £15,000 in total. Furthermore, the whole sum could be in cash unlike before where only half of the limit could be saved in cash and the rest in shares. Also, the 10p tax rate for savers will be abolished. CLASS 2 NIC From April 2016, Class 2 National Insurance Contributions (NIC) will be collected through self-assessment. CHILD-CARE HELP Parents paying 80% of childcare costs of up to £10,000 per child, aged up to 12, to a registered provider will get the remaining 20% tax-free from September 2015. NEW TRANSFERABLE TAX ALLOWANCE From April 2015, there will be an introduction to a new transferable tax allowance for married couples and civil partners. PENSION CHANGES All tax restrictions on pensioners' access to their pension pots to be removed, ending the requirement to buy an annuity. The taxable part of pension pot taken as cash on retirement to be charged at normal income tax rate, down from 55%. There is an increase in total pension savings people can take as a lump sum to £30,000 By Wilson Law at Tax Affinity Accountants Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered to be small business experts helping and supporting business in the UK. They regularly help new business start up and provide valuable support for new businesses. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends. |

Various AuthorsOur experienced accountants and tax advisers provide valuable insights into practical every day questions and issues. Archives

March 2024

Categories

All

Ask your own question: If you would like to have a tax related question answered here, please send your question to [email protected]. |

RSS Feed

RSS Feed