Some landlords wrongly think by not declaring their property to HMRC they are safe! As experts in property tax we often get asked by clients who are landlords and property developers how to save tax - especially so as the cost of letting a property rises year on year.

With our experience and special insider knowledge that HMRC in 2014 - 2015 is especially looking at checking landlords who are not declaring the correct rental income and correct capital gains on second homes. This is something that is becoming more important as people realise it is harder and harder to hide their untaxed property incomes. Landlords or their accountants are required to fill the the land and property section on their self assessment tax return showing all the rental business income they have made and as many want to make sure they pay the least amount of tax possible. We have have created a simple list to help guide you. Here are Tax Affinity Accountants top tips to save property tax. 1. Claim for all your property related expenses. Its important to make sure you claim for all your expenses when submitting your tax return. These should include: • Travel costs incurred when travelling back-and-to the investment property • Estate Agent or private advertisement costs • Mobile or landline telephone calls made (or text messages sent) in connection with the rental property • Payments for safety certificates eg Gas Safety • Bank charges (i.e. overdraft, interest on mortgage) • Professional fees e.g. Architect, Solicitor, Accountant etc • Monthly payments to property investment related products and services eg Insurances etc 2. Dividing your rental income between partners. A top tip is to consider putting your buy-to-let property into joint named ownership. Then the total income can be divided into each person's income and multiplying the personal allowance claimable on the income. 3. Claim all empty period expenses. Often there are periods between lettings that the buy-to-let property is empty and the owner has to pay for council tax or utlity bills. These should be noted and claimed. 4. Claiming the home office allowance. £4 per week (ie £208 per year) can be claimed for the use of your home to manage and run your rental property income. This amount can be claimed without evidence and more can be claimed if it can be justified. 5. Interest and finance costs. Most properties are on mortgages and the interest part of any mortgage is claimable as an expense. So if you have an interest only mortgage then the whole amount is claimable per month paid. Often landlords also forget to claim for money borrowed from friends or family or taken on a credit card or personal loan for the buy-to-let property and the interest on these can also be claimed. The principal can only be claimed when selling the property against capital gains tax. 6. Dont forget to carrying forward loss from previous year Most of the time a new buy-to-let property will not breakeven in its first year and so many landlords have significant rental losses for that year. Then when they start to make income from the property most forget about this loss which can be offset against the current years income. This could even mean no tax to pay in the current year if the losses are great enough. This requires detailed technical knowledge and so any lanldord in this situation should contact an experienced accountant such as Tax Affinity Accoutants. 7. Capital gains avoidance If landlords who are planning to sell their property, need to plan months or even a year ahead to increase their options of minimising capital gains tax which will arise on the sale of the property. This is usually best done getting expert advice from an accountant experienced in tax and property such as Tax Affinity Accountants. What top property developers and landlords know that mostly the fees paid to a good accountant are far less in comparison than the tax he/she will save you. 8. Wear and tear allowance Letting your property as furnished as opposed to unfurnished can allow you to claim up to 10% of the gross income as a valid expense for the upkeep and repair of furtniture in the tax year. 9. Make Sure to avoid HMRC interest and penalties Sound obvious but far to often, we see penalties and interest charges for late filing of tax returns and missed deadlines for documents to HMRC. The deadline for a paper return to HMRC is 31st Oct and online 31st Jan each year. Please also not that landlords will not be able to submit their return electronically if there are any capital gains elements on the return. ie the sale of any property. An experienced accountant needs to be contacted for this purpose which if knowledgable enough could ensure all capital expenditure is claimed to reduce the capital gains liability as low as possible. By Andrew at Tax Affinity Accountants. Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered to be property tax experts helping and supporting ladlords across the UK. They regularly help new landlords and property developers and provide valuable ongoing support. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

0 Comments

How the queen’s new polices will affect businesses around the UK (big/small)

Today I will give you some insight into how the queen’s new polices will affect businesses around the UK (big/small). There are various topics from the queen’s speech that would affect businesses around the UK (big/small). I will discuss each one in detail to give you an insight before it comes into play. ''To build a stronger economy we must support smaller businesses to compete within their sector. Furthermore, we should ensure they should not be disadvantaged by those who do not play by the rules (larger companies)''. The main elements are:

We must protect public revenues by tackling avoidance and also help hard working taxpayers by simplifying the collection of class 2 National Insurance contribution (NIC) paid by the self-employed. Simplifying the NICs paid by the self-employed:

Public sector land assets are to be transferred directly from arms-length bodies to the homes and communities agency, reducing bureaucracy and managing land more efficiently. Furthermore, guarantee that future purchases of land owned by the homes and communities agency and the Greater London authority will be able to develop and use land without being affected by easements and other rights and limitations suspended by the agency. Land registry would transfer statutory responsibility for the local land charges register and delivery of local land charges searches to the land registry, supporting the delivery of digital services and broaden land registry’s powers to facilitate it to grant information and register services relating to land and other property. The adjustments to the pension tax rules (as announced at the budget) are to help people get on by giving them greater independence and choice over how to access their defined contribution pension savings. The main elements are:

Other measures that will effect businesses and indviduals are as follows:

By Tahir Malik at Tax Affinity Accountants Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered in the Finance Industry to be the experts in all types of Accounting and Tax issues. Helping and supporting businesses and individuals throughout the UK, Europe and USA. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

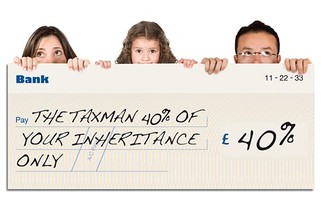

Plan Plan Plan ahead to save Inheritance Tax

Saving Inheritance tax

Inheritance tax can be a tricky issue to deal with for most people but it is generally considered a “voluntary tax” as good tax planning can greatly reduce your inheritance tax liability or erase it completely. Assets exceeding the current inheritance tax threshold of £325,000 (for tax year 13/14) are taxed at 40%. That’s basically half of your excess assets going straight to the government and not to your loved ones. This is why inheritance tax can be extremely costly for those who have not done sufficient planning. Fortunately, there are many exemptions and allowances to utilise which would significantly reduce the amount of inheritance tax you have to pay. Here are a few things to consider that can help you save some inheritance tax:- Make a Will Making a will allows you to know that your estate is divided exactly as you want it to be when you die. In the absence of a will, people that you wish to benefit from your estate such as an unmarried partner may not be entitled to any share in the event of intestacy. What is a gift? A gift is something of value given unconditionally to someone without any reservations. The biggest asset that most people are in possession of is their house. However, giving away your house yet trying to live in it may allow HMRC to invalidate the gift as genuine and apply tax on it. Give away sooner Majority of gifts you make are classified as “potentially exempt transfers”. If you survive more than seven years after making the gift, no inheritance tax is due on that gift. The amount of tax can be reduced depending on how long you lived after making the gift due to taper relief. Gifts made less than three years before death have no reduction in tax. If the gift was made three to four years before death then tax is reduced by 20%. This increases by 20% for every extra year the donor lives up to seven years where the whole amount is exempt. Therefore it can help relief some financial burden on your death estate if you make gifts sooner rather than later. Allowances to take advantage of You can give away gifts worth up to £3,000 in total per person every tax year and these gifts will be exempt from inheritance tax when you pass away. Any unused part of this annual allowance can be carried forward to the following year, but if you don’t use it in that year, the carried-over exemption expires. You can also give up to £5,000 to your children when they marry as a wedding gift. Grandparents can give up to £2,500 and others up to £1,000. Regular Gifting Regular gifting can dramatically reduce your inheritance tax bill as long as they meet the following criteria: they must be from your income, they must be regular and they must not decrease the standard of living of the donor. Be generous on birthdays Gifts under £250 to any recipient per tax year are exempt from inheritance tax. This means that it might be worth giving your boy a big birthday present even if he’s been naughty as it helps reduce the tax bill. Gifts to charities and political parties are tax-free It’s good to know that any donations you make to charities or political parties are inheritance tax free at least. Getting Tax Advice While it is generally more economical for you to do things by yourself, if you have sizeable assets then seeking professional tax advice is well worth your money. You may end up paying a few hundred pounds to potentially save over hundreds of thousands of pounds. I’m no bargain hunter but that sounds like a good deal to me. By Wilson Law at Tax Affinity Accountants Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered in the Finance Industry to be the experts in all types of Tax including Inhertance Tax. Helping and supporting business and individual throughout the UK, they regularly help people with their Inhertance tax issues. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

A good accountant should save you far more money than they ever charge

Many business owners wonder whether hiring an accountant is worth the extra expenditure. From the viewpoint of an accountant, it would be hypocritical for me to say that you’re better off doing all the accounting work yourself. In some respects that may be true. You may save some money by not having to pay accountancy fees. However, over the long run, you will probably realise that the time spent on dealing with your tax affairs and managing the company accounts can be used much more productively. Image the time is used earning a few more sales per week compared to being counted as dead time doing admin.

The phrase that time equals money is heard commonly. Not only do accountants save you both time and money; they also become an invaluable asset to your business. On that can become worth so much more than a simple financial cost. Here are a few things that we can add real “value” to your business: Proper Book-Keeping Keeping your financial records organised and up to date is the most important factor to dependable financial statements. But why hire an accountant as opposed to a book-keeper. Unlike the duties of a book-keeper, an accountant can help interpret the results, offer professional advice and present the financial statements in a format that allows decisions to be made by business management. You would get a greater insight to your business and be able to plan ahead using forecast estimates. Allowable Expenses Many business expenses are deductible. However, most of the rules and regulations change on a moving basis and vary from business to business. A good accountant will always be updated on the changing laws and regulations. And therefore should be saving you far more in paying less tax per annum than he/she should ever charge in fees. Their knowledge and experience will add real value to your business. Compliance There are standard formats for filing your accounts and various other tax returns to HMRC. An accountant can ensure that the relevant information is submitted to HMRC in the correct format before the due date. If there is one thing that panics business owners more than anything is a letter from HMRC about a mistake in their tax return and accounts. An accountant can deal with any issues in that regard in an efficient manner. So many clients turn to an accountant after having incurred fines and penalties that they often wonder why they just didnt do it before. Tax Advice Being aware of tax savings does not necessarily translate to actual tax savings. An accountant’s job is not only to tell you how much tax you owe but how you can save tax. The accountant should work with you throughout the year and offer advice on how to operate your business in a manner that will provide the most tax savings. This can save you substantial amounts of money in the long run - again far more than he/she should ever charge. Business Consulting Business advice from an accountant can help grow your business. They can assess your current problems and provide solutions to fix them. Or if your business just needs a fresh but experienced perspective on how to expand. The advice can be on inventory management, risk management, lease and buy decisions, internal controls or pricing strategies, HR issues, mergers, sales and takeover of the whole business even. Develop a Business Relationship Lets be clear in our extensive experience there are a lot of arrogant and selfish accountants out there. People regularly come to us saying their previous accountant was not doing enough and was charging them for every little thing. A good accountant wont mind spending as much time as you need to make sure you get all the help and support required. Their fees should be transparent and fixed, with no surprises. Speaking with an accountant can get you the advice in regards to your tax affairs or business operations. He/She can help identify problems in your financial statements and consult you about it. They can often with a little direction from you, supply you with the ideas and expertise that you desire to push your business to places your imagined. After all the biggest businesses in the world trust some of the biggest firms of accountants to help them with their plans for global expansion and growth. By Wilson Law at Tax Affinity. Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered to be small business experts helping and supporting business in the UK. They regularly calculate and submit tax returns, year end accounts and so much more for their clients peace of mind. Whilst always ensuring great value for money service. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.  No matter what type of property you have you can save on taxes! Properties have always been a relatively safe and sound option for investment. As a landlord, renting out your property can offer an alternative source of income in the form of rent and potentially give a good return on the initial investment through capital appreciation. However, if you’re looking for huge returns over a few days then property investment is unlikely to be your preferred choice. Nonetheless properties have historically been a low risk investment and have provided modest returns over the long term. Here are a few things to consider if you wish to maximise your rental income:

Deducting Allowable Expenses You can reduce the amount of rental income that is taxable by taking advantage deducting allowable expenses. There more common expenses you can deduct are:

The costs should be wholly and exclusively incurred as a result of renting out the property. If a part of the expense meets this condition then that part can be deducted from income. Cost comparisons Saving costs can only have a positive effect as expenses are the only thing eating into your rental income. Try reviewing your costs on an occasional basis (once a quarter) and you may witness bargains that could help you save a lot of money. Service providers tend to offer sizeable discounts to new customers but only have stagnant prices for existing customers. Getting quotes from different companies that offer the same service can sometimes amaze you at how wide the price range can be. Just be sure you don’t jeopardise the quality of services just to save a few pennies. Annual Investment Allowance Expenses of a capital nature are not deductible. You cannot deduct from income the cost of the property you are renting out, expenditure that adds to or improves the property or the cost of renovating a property from a state that cannot be rented out. However, capital spending can be deducted using the Annual Investment Allowance. From 1st January 2013 (until 1st January 2015), you can deduct up to £250,000 a year for many types of capital spending using the Annual Investment Allowance, such as commercial vehicles, business furniture, computers, machinery and tools. It would be beneficial to take advantage of the temporary rise in the Annual Investment Allowance as it is likely to revert back to around the limit of 2012/13 (£25,000) after January 2015. Landlord’s Energy Savings Allowance (LESA) Until April 2015, an allowance of up to £1,500 per let residential property can be claimed for the cost of loft, wall and floor insulation, draft proofing and hot water system insulation. The LESA was introduced to encourage landlords to improve the energy efficiency of let residential properties. These expenditures are usually not deductible from taxable income and are not eligible for capital allowances. Wear and Tear Allowance or Renewals Allowance For fully furnished properties, a wear and tear allowance can be claimed for furnishings such as beds, carpets and appliances. The allowance is 10% of the net rental income (gross rent minus utility bills, service charges and council tax) you receive from these properties. With the renewals allowance, you can claim expenses of any furniture as you replace them. Any money you make from the disposal of the asset must be deducted and the cost of any improvements (e.g. an upgrade from a washing machine to a washer-dryer) Note that you can only claim either the Wear and Tear Allowance or the Renewals Allowance but not both. By Wilson Law at Tax Affinity. Tax Affinity Accountants are considered in the market to be experts in Tax and Accountancy in the UK. Based in Kingston upon Thames they have clients right across the UK as well as Europe, Middle East and North America. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

Where to invest in the current economic climate- Property versus Shares There is much debate regarding the merits and fallbacks of investing in property versus shares. Traditionally, investments in property have been seen as more stable whilst stocks are far more volatile. Either way, with the retail banks continuing to offer painfully low interest on savings, coupled with high rates of inflation, investors are looking to achieve higher rates of return on their capital. This article gives an outline of the respective issues surrounding both methods of investment. Property Figures for August 2013 show a sharp rise in UK property prices, with the average UK property now worth 3.5% more than a year ago. Economists have pointed towards increased consumer confidence, due to the economic recovery, as a key driver behind rising house prices. Equally, the Government’s Funding for Lending (FLS) scheme and the Help to Buy scheme have gradually improved credit availability. While rates offered by the banks for your savings remain low, property investment can offer a higher return on your capital. Buy-to-let investment is a very sensible option as it offers two potential returns on your investment. Firstly, assuming you find tenants rapidly, you will enjoy a regular stream of income from rent. And secondly, provided you invest in the right property, you have an appreciating asset that can earn you a healthy profit should you look to sell in the future. Furthermore, unlike with shares, property allows you to leverage up your investment. This can be simplified as follows:

This is a hugely simplistic example which discounts some of the costs of property investment but it does highlight the benefits of leverage in property investment. Issues with Property Be careful to choose your location wisely as this will be central to the future value of your property and the rents you can command. Inevitably, the surrounding suburbs of London are extremely popular as they can allow for easy commutes whilst being priced more reasonably than equivalent properties in more central locations. Kingston upon Thames, Ealing, Hackney and Merton are all prime examples of this. Equally, it is worth considering that this unprecedented period of record low interest rates is bound to come to an end as the economic recovery gathers momentum. If interest rates rise then this will make mortgage repayments a far greater burden on potential property investors. Shares Investing in equities is another method for achieving greater return on your capital. The FTSE 100 index has seen a notable recovery since the financial crash around 2008 and now shares are becoming a more appealing investment once again. However, investment in shares requires more industry-specific knowledge in order to outperform the market and thus it may be advisable to invest in an Investment Fund or an Investment Trust:

Tax Implications for Investments in Property and Shares As with all investments, profits made will be liable for Capital Gains Tax (CGT) so this is worth considering before you invest. However, there are certain methods to avoid CGT. For example, you may wish to put your property or shares into a trust. Equally, stocks and shares ISAs can be used to shelter equity profits from CGT. Also, utilise your full tax-free allowance by splitting your assets with a spouse so as to minimise your tax bill. Verdict Overall it is probably fair to say that the optimal investment strategy would involve both property and shares. Bricks and mortar provide a more reliable investment option whilst the riskier option of share investment can reap higher rewards. However, with the FTSE 100 at extremely high historic levels one might argue that property can provide more reliable profit margins. By Tom Hoadley. To read more interesting articles visit www.taxaffinity.com/blog. Tax Affinity Accountants are expert tax and business accountants based in Kingston upon Thames. They provide a comprehensive range of services to businesses across the UK. To contact them visit www.taxaffinity.com. |

Various AuthorsOur experienced accountants and tax advisers provide valuable insights into practical every day questions and issues. Archives

March 2024

Categories

All

Ask your own question: If you would like to have a tax related question answered here, please send your question to [email protected]. |

RSS Feed

RSS Feed